How Connected Vehicles Will Impact the Insurance Industry – Grape Up

By 2023, there will be about 350 million related automobiles on the street. What can the insurance policies market do about it? It turns out that really a bit, as automotive businesses, introducing the latest technological advances, are enabling new ways to blend driver habits. This is of good value in the context of generating features, but not only. At stake is to maintain the placement and competitiveness in the subject of motor insurance policy.

The automotive and car insurance policies industries are transforming

The automotive current market is presently enduring alterations driven by innovative technologies. Extra typically than not, these are primarily based on the application-outlined car (SDV) pattern.

If the auto is geared up with embedded connectivity, it is in a position to provide extremely specific vehicle and driver actions info, this kind of as:

● unexpected acceleration or braking,

● having sharp turns,

● peak activity times (nighttime motorists are extra vulnerable),

● ordinary speed and acceleration,

● executing hazardous maneuvers.

BBI & UBI and ADAS

Behavior-centered (pay-how-you-generate) and usage-based mostly insurance policies – UBI – (shell out-as-you-travel) are the foreseeable future of automobile insurance coverage courses. In the meantime, as automobiles turn out to be smarter, extra connected, and automated, insurers examine not only the driver’s conduct but also the car s/he is driving. This evaluation normally takes into account, amongst other items, the sum of innovative driver support methods (ADAS) that have an impact on the security of the vehicle’s occupants.

Autonomous vehicles

And Deloitte analysts observe that self-driving (AV) cars, which are an intriguing novelty now but will in time be a standard on par with human-pushed motor vehicles, are also very likely to force fundamental adjustments in insurers’ product or service ranges, as in the danger evaluation, pricing, and enterprise models.

Connected vehicles

Transform is now occurring, and it will grow to be even more pronounced in the yrs in advance. IoT Analytics predicts that by 2025, the total selection of IoT products around the world will exceed 27 billion. Plus, industry experts predict that there will be 7.2 billion active smartphones and more than 400 million related automobiles on the highway all through the exact period.

This all evidently shows that we are in an totally various reality than we were just a several or a dozen decades ago. Car insurers need to have to comprehend this if they want to manage their foothold.

Telematics systems are an obvious action into the future of the insurance coverage field

Insurance policy companies have been providing utilization-centered and actions-based goods for yrs based mostly on information from possibly further units or cell applications. This is a quick-rising merchandise location since the UBI marketplace is predicted to be well worth far more than $105 billion in 2027, up 23.61% every year.

The ideal position in this arena is attained by corporations that begun investing in telematics engineering early and now can acquire delight in well-created telematics products and solutions.

We are speaking about brand names these types of as Point out Farm®, Nationwide, Allstate, and Progressive. Yet at the very same time, corporations that deemed telematics a passing trend and consequently didn’t invest in it lost a extremely big amount of current market share. The final result? Now they have to capture up and race to preserve up with the competition.

TSPs realize the likely of linked vehicle information

Insuring providers are not the only types who understand the importance of implementing their telematics-based methods. Telematics providers companies fully grasp that worth as properly, so they spend in constructing out new abilities of their products.

This is the circumstance with GEICO, the next-largest automobile insurance company in the U.S. (ideal soon after Progressive). As Ajit Jain, vice president of Insurance plan Functions at Berkshire Hathaway promises: GEICO experienced plainly missed the business enterprise and have been late in phrases of appreciating the worth of telematics. They have woken up to the reality that telematics performs a significant job in matching amount to hazard. They have a variety of initiatives, and, ideally, they will see the light-weight of working day prior to, not way too extensive, and that’ll permit them to catch up with their competition, in conditions of the difficulty of matching amount to hazard.

Telematics corporations see opportunity in partnering with the insurance policies marketplace

Insurance coverage businesses are not the only kinds who acknowledge the great importance of employing new data-driven engineering methods. The romantic relationship is two-way, as telematics marketplace representatives, in flip, are prepared to devote in collaboration with insurers and put the customer from this market sector first.

For case in point, Cambridge Mobile Telematics (CMT), the world’s most significant telematics company, has lately declared the expansion of its proprietary DriveWell® telematics platform to networked automobiles. Their flagship software package has formerly gathered sensor data from tens of millions of IoT gadgets, together with smartphones, tags, in-car cameras, 3rd-get together gadgets, and many others. From now on, that scope continues to grow by specially such as related autos to make a unified view of driver and vehicle behavioral risk.

This synergy of all acquired facts is predominantly devoted to clients in the auto coverage sector, who achieve insight into what is happening on the road and powering the wheel. As Hari Balakrishnan, CTO and founder of CMT describes: There is a wave of progressive IoT details sources coming that will be vital to comprehending driving danger and reducing crash costs. CMT fuses these disparate info resources to create a unified view of driving.

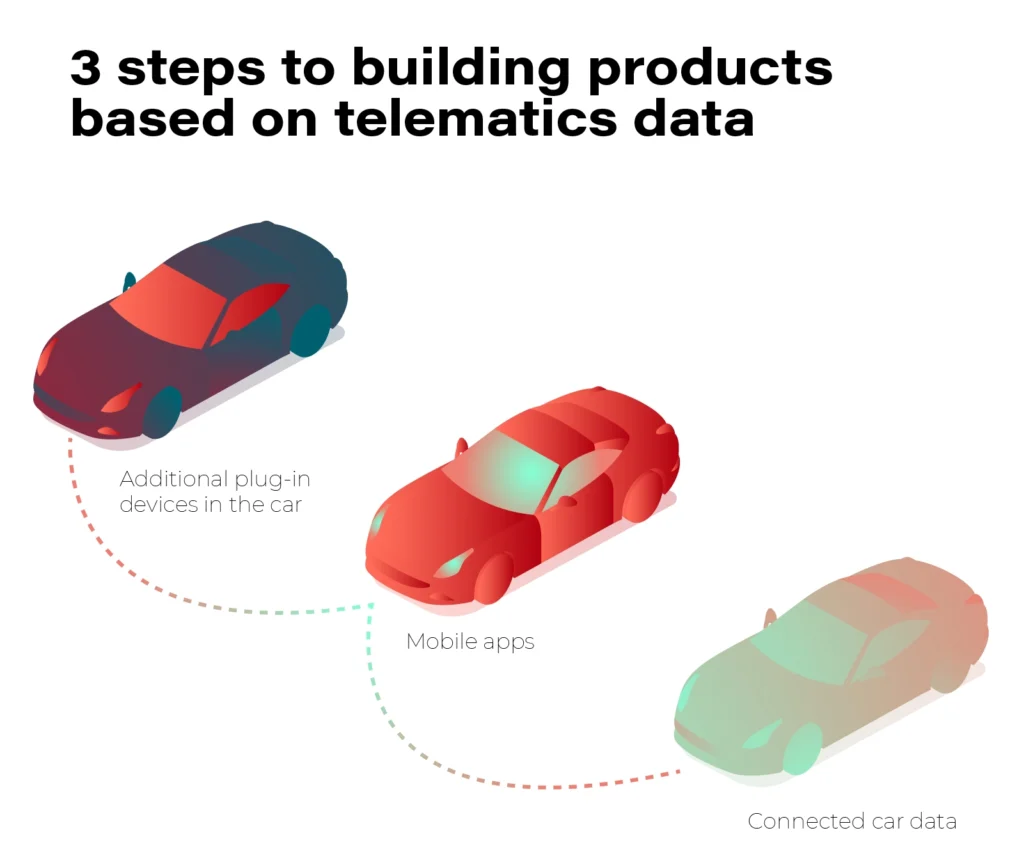

Recent UBI alternatives can be flawed

Current techniques of info selection for insurers also count on modern technologies, but these can be unreliable. All three approaches have their disadvantages: equipment plugged into the On-Board Diagnostic (OBD) procedure, smartphone applications and tags stuck to the windshield.

The very first technique supplies insight into the driver’s precise habits information, downloaded specifically from the engine control module (ECM). Weaknesses? The simple fact that OBD-II equipment are constrained to the details observed in the ECM, for illustration, whilst people from other car elements remain inaccessible.

In this respect, cell applications are unquestionably much better, furnishing insurers with a uncomplicated way to start their possess telematics-based system. . In addition, info is collected each time the consumer drives the motor vehicle. The disadvantage, having said that, is that the software does not connect directly to the vehicle’s programs. As a result, the data factors are issue to a margin of mistake, and it also comes about that the computerized driving recognition fails and incorporates in the scoring journeys as a passenger in another vehicle, for example.

Bluetooth-primarily based tags, which is the previous option explained here, are installed on the vehicle’s windshield or rear window. Like cellular apps, the tags have no direct link to the vehicle’s systems and are thus prone to bugs.

The conclusions are obvious

As a result, there is a whole lot to propose that if an insurance provider is searching for definitely dependable technology, it need to opt to use embedded telematics, or information. This is what permits dynamic and, over all, unconditional information collection to reliably assess the chance involved with person shoppers.

The knowledge despatched by connected autos is extra correct, more comprehensive, and in a lot bigger portions in comparison to other answers. And this lets insurance policy companies to better have an understanding of clients and their conduct and, centered on this details, supply goods that are better suited to their demands, as effectively as much more successful.

Industry insiders really do not have to have a great deal convincing about the benefits of telematics and linked cars more than other driver knowledge selection remedies. Info from automobiles connected to the network are promptly obtainable. Of training course, you can enrich it and give it context by employing facts from smartphones, but in most circumstances, it is not even important. So why spend in something unreliable, which by definition has vulnerabilities and does not meet 100 percent of your demands, when you can decide for a more complete technologies that gives additional characteristics correct from the commence.

Appreciable importance of related auto knowledge for the insurance coverage industry

Connected car or truck knowledge is the subsequent action in developing the ultimate telematics-dependent solutions. It is obtained without having the need to have to put in added components. All it will take is a auto user’s consent to use the info, and then the insurance policies enterprise obtains the details instantly from the OEM.

The data attained from UBI cars can be employed productively and all stakeholders advantage: insurers, as they achieve a much better understanding of their customers and can improved assess threat OEMs, as it allows them to monetize the details and ultimately shoppers, who acquire a superior, far more personalised present this way. J.D. Electrical power factors out that 83% of policyholders who had optimistic statements working experience renewed their procedures, in comparison to only 10% who gave negative opinions.

In addition, this sort of dependable information serves not only to improve the profitability of an insurance plan portfolio, but also to strengthen street security. Insurers can provide incentives that will really encourage their clients to continuously strengthen their driving model and maximize their care for on their own and other highway end users.

Even now, current market leaders who fully grasp the benefit of investing in innovation are supplying their buyers the chance to share knowledge from connected cars for UBI/BBI needs. A person illustration is the Point out Farm® brand, which features special discounts primarily based on driving actions. The driver’s on-the-highway actions ( sharp braking or no braking, quick acceleration, swift turns) and driving mileage are instantly despatched to the facts supervisor just after each and every vacation, so be sure to enable knowledge sharing and area services on your saved car. This info is employed to update your Generate Harmless & Conserve discount every time you renew your policy. The safer you drive, the far more you can preserve.

Similarly, Ford Motor Corporation is significantly shifting toward making use of driver data in UBI courses dependent on connected motor vehicles. To that close, the automotive huge has partnered with a mobility and analytics manufacturer. Their joint venture is expected to empower drivers with far more control in excess of how a great deal they spend for their car insurance coverage. Drivers can voluntarily share their driving facts from activated Ford motor vehicles with Arity’s centralized telematics system, and it will then be delivered through Arity’s API. Drivesight® to insurers. The received hazard index can be made use of to price car insurance policy by any collaborating insurer.

Presently, related vehicles are only just one alternative, as lots of insurance providers are nevertheless applying, for illustration, cell apps in parallel. Even so, we can already see that the craze of using CC data is existing on the market place and the selection of corporations supplying this kind of an solution to their shoppers will improve. This is a thing to be reckoned with.

Major gains

For insurers, the positive aspects are tangible. According to Swiss Re, with 20,000 claims managed for each calendar year, the ordinary cost savings just after utilizing the over technologies amounted to 10-30 USD per assert.

Telematics also aids to suppress so-termed claims inflation. Increasingly state-of-the-art cars are equipped with advanced parts, which can be costly to switch. Fortunately, today’s insurer has the skill to make its individual strategy centered on the shifting value of spare elements and injury history for significant car or truck styles. This permits them to establish new pricing that consists of inflated compensation prices.

The quicker, the better

Leveraging facts and analytics based on synthetic intelligence is assured to generate development. Expanded sources of information enhance the client expertise and aid streamline operational procedures. The gains are hence obvious throughout the complete price chain. We can confidently say that hardly ever just before in heritage has engineering been so intertwined with the insurance plan sector.

That is why all insurance coverage firms should commence functioning on incorporating linked car or truck info into their programs now. The quicker they do, the much better positioned they will be when these motor vehicles become mainstream on the road. Right after all, the share of new motor vehicles with crafted-in connectivity will access 96% in 2030.

Which is what Evangelos Avramakis, Head Digital Ecosystems R&D, Swiss Re Institute Investigation & Engagement advises insurance businesses to do: Setting up modest then scaling quickly could be a good approach (…) There is so considerably you can do with info. But you have to have to just take a unique method, depending on irrespective of whether you want to make improvements to claims processing or build new merchandise. Conversely, this is what Nelson Tham, eAdmin Pro Asia, P&C Enterprise Administration, thinks about implementations: When an SME thinks about digitalization, it intimidates them. But it require not be the scenario if we start compact. They can start off by reviewing their inner procedures, see how knowledge flows, convert that into structured facts, then examine this data for a lot more significant insights.

How the insurance policy marketplace need to strategy the matter?

Insurers really should start by answering essential concerns like: wherever linked auto data will provide the most price for my company? What inner capabilities do we have and will need? Do we have the essential infrastructure, process and capabilities to leverage linked car or truck info? What investments in know-how are essential to produce on our plans?

Last of all, they want to think about whether or not they can much better and quicker achieve those aims by building expected abilities in-home or performing with partners.

A excellent enterprise and technology spouse for the coverage business is fundamental

Working with linked auto knowledge is not that uncomplicated. It necessitates know-how and the appropriate technological innovation track record, as properly as finding the suitable partner to collaborate with.

A effectively-matched associate will help alter the latest running product, by combining automotive and technological innovation competencies and at the exact same time understanding the specifics of the insurance policy market. Some procedures just have to be carried out in a detailed and holistic way.

At GrapeUp, we assistance put into practice new ways to an current tactic. Working at the intersection of automotive and insurance plan, we focus in the systems of tomorrow. Get hold of us if you want to strengthen your enterprise efficiency.